Investors and traders have been anxiously waiting for an opportunity to return to equity markets with full strength, especially to the European markets that have been suffering the most since the beginning of the financial crisis. While Germany, the US and the UK have performed exceptionally well from the crisis bottom, Spanish and Italian equities are still struggling. In fact, last week, returning exactly to their March 2009 nadirs of three years ago in contrast to a doubling of index levels of the former three regions. Is this a fair reflection of their economic problems that will last? Or, are these markets now exceptionally undervalued – a stance opined in this blog by our editor – Richard Jennings?

Italian and Spanish Equities Have Been Struggling

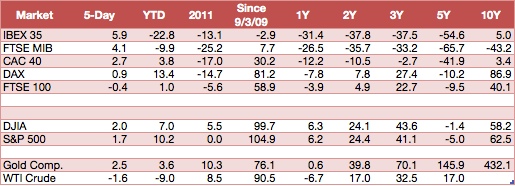

With the help of the table below, we can easily spot an abysmal difference between Europe and the US and further, between central Europe and the peripheral countries. Excluding Germany, equity performance has been much better in the US than in Europe during the last ten years. While equities rose around 60% during that period in the US, equity returns have been flat in Spain and France and, frighteningly for proponents of the long term buy & hold stance, negative in Spain. If we look at each of the last three & five years, or at almost any other interval, the story is the same. US and Germany have outperformed everything else with the UK detaching from other European countries but still not enough to reach the top.

Performance table

The Italian index FTSE MIB shows the worst performance of all and lost one quarter of its value during 2011. The IBEX index has also been performing poorly, however a little better than its Italian counterpart. Both haven’t recovered since the bottom observed on March 9, 2009 as the following chart clearly shows.

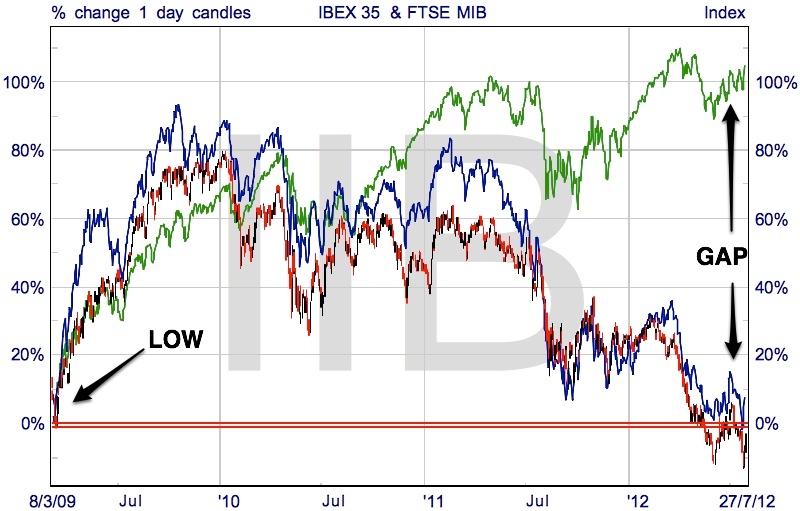

IBEX (red) & MIB (blue) relative to S&P500 (green) since March 2009

Mario Draghi’s Words

Last week, Mario Draghi seemed to ride to the rescue with his unexpected comments in which he stated that that he was prepared to do “whatever it takes to save the euro”, to make absolutely sure the market got the message, he elaborated with further strong words – “believe me, it will be enough”. Since that day, the blue touch papaer has been well & truly lit underneath Italian & Spanish equities in particular – a position called for by this magazine just 24 hours befor Draghi’s remarks.

Some observers now expect the ECB to commence further monetary easing, starting this Thursday at the ECB press conference. Other commentators are a little more sceptical and believe Draghi’s remarks to be nothing other than further politically motivated rhetoric, adding to the already huge amount of it that has emanated from the Eurozone since the crisis began. While we wait for the exact path of action, let us take a look at two particular markets: IBEX and FTSE MIB.

While the whole of Europe would benefit from action taken by the ECB, Italy and Spain are the two countries that would benefit the most as direct ECB action would alleviate the pressure these countries currently have on their debt burdens.Those markets rose between 10and 15% in the last five days (last week). Just a few words from Mario Draghi, and those indices shot up like a rocket. If Draghi acts next Thursday, these markets will boom.

Digging Inside the Economic Data

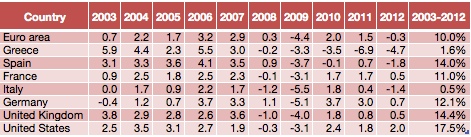

Just why have Italian and Spanish equity values been so depressed, especially Italy? Are we now sitting at a multi -year bottom or is there more downside risk? The economic data may help understand the reality behind these two countries. The following table shows the ‘real’ GDP growth rates that have been experienced in the last ten years for some EU countries and the US.

GDP Data – 10 year

While the EU grew 10% in the period, the Italian economy stagnated, just growing 0.5%. It grew less than all the others between 2003-2007 and then suffered the most in 2008. With the lack of growth all over Europe and with all the austerity measures still to be implemented, it will be tough for Italy to outperform at the economic level in the near term. It’s economy was not able to grow significantly, even when the world was in expansion, and so indicating that it still needs many reforms to be implemented.

The Spanish case is much different. Spain has been growing more than the EU as a whole, indeed on a par with other economies including the US. Spain has been one of those countries that has suffered the most due to the housing bubble that has effectively put its banking sector, particularly the Cajas, in a state of bankruptcy. Credit was tightened and unemployment rose quickly from 8.3% in 2007 to the current, astonishing, 24.6% rate. In less than four years, the deterioration has been huge. Indeed, on some measures, the deterioration has been of the magnitude that the US suffered during the depression of the early 30’s. But, this economy does have the necessary flexibility to grow fast and recover, if some steps are taken. A concerted measure of intervention by the ECB to stabilise debt markets would help the country finance its debts on much more favourable conditions and so help stimulate business activity again. This would be a real cue for investors return to the equity market.

Enter or Wait?

In terms of long term investing, both Italian and Spanish equities are at an excellent point to be considered as an investment opportunity. They have suffered disproportionaely during the last ten years and have now missed the recovery experienced by other markets since 2009. The Spanish economy has been growing more than the Italian and it is better positioned for a take off, but with the FTSE MIB currently quoted at half its 2002 value (without factoring in inflation), it is a real temptation too.

10 year chart of Ibex (red) & MIB (blue) & S&P 500 (green)

For spread betters, the opportunity is a little different. Much action still has to come from European leaders and, markets will continue to yo yo in the meantime until a clear solution to the Eurozone problem arises. The volatility experienced by the FTSE MIB and the IBEX has been huge in recent months, and the leveraged nature of spread betting doesn’t allow for much downside unless you keep your account well funded – a point this magazine continually hammers home.

An alternative approach in spread betting would be to buy some medium dated Call options. A call option has limited downside and will allow you to make money even if the market goes down before taking off. In volatile markets this is key. Options may also be a great tool for this week since increased volatility is expected with the FED, the BOE and the ECB all meeting on monetary policy. Of course, simply entering into a modestly leveraged long position on the MIB or Ibex allowing you to ride out any pullbacks is another way to play this story.