In the not-too-distant future, it is quite possible that the combination of the letters AA will not refer to Alcoa Aluminium, or indeed “Alcoholics Anonymous”, but quite possibly the bold monetary experiment that has been undertaken by Shinzo Abe – the “Abenomics Adventure”!

Since being newly re-elected at the end of 2012, Japanese PM Shinzo Abe has pursued his election promise to drive prices higher in Japan after 20 years of on/off deflation. Thus far however, this has come at a substantial cost for his own population and, as a side effect, hit some of Japan’s trading partners. Sadly for the unemployed youth of Spain, Greece and Portugal, Europe is at the top of this list. The depreciation of the Yen is crimping her trade partners from a trade competitiveness basis and in the process boosting the profits of her own exporters.

A peculiar but, if one thinks about it, a perfectly logical side effect of the money printing exercise, is that the Japanese people are returning to gold again as a way to try and stave off potential runaway inflation should the money printing be ratcheted up once more, and which looks ever more likely…

According to the latest economic data, it appears that the Abenomics plan is working with prices for many goods right across the board in Japan now rising. The latest numbers point to an annualised inflation rate of around 1.5%, – a figure that recent memories have no recollection of. Unfortunately for Japanese politicians however, household spending has been declining with many economic commentators expect this to worsen with the imposition of the latest sales tax increase – a measure that when last introduced, properly crimped the Japanese consumer.

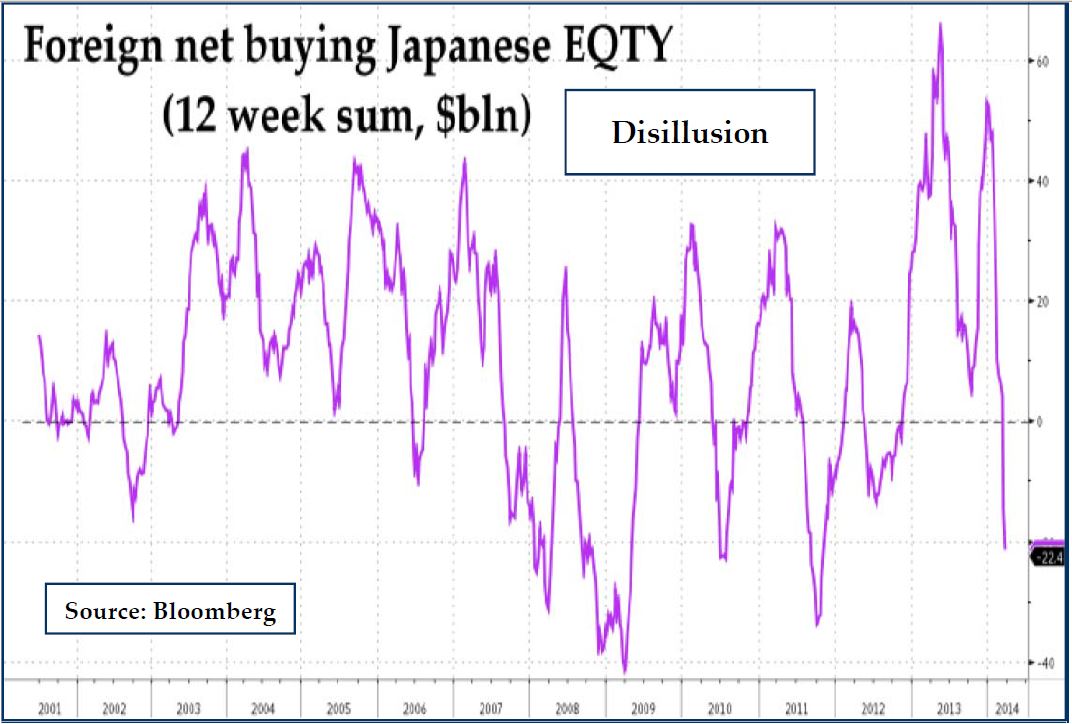

All this has not gone unnoticed by international investors with reports in recent days that foreign investors have been selling stocks at the “fastest pace in a decade” (see chart below). Regular readers will know that when everyone runs one way that here at Titan we get ready to run the other! In fact, the ratio of speculative bets by hedge funds and other investors reached the highest in 5 years last week. At the end of March, data from the Japanese Finance Ministry revealed a net $11bn of stock was sold with the ratio of short sales rising to nearly 40% of all sales in recent weeks. That’s some contrarian opportunity that is being presented…

Back to the economics… when inflation rises, the cost of “holding” money of course increases such that the incentive for consumption simultaneously increases. What Abe didn’t consider was that instead of consuming domestic products, the Japanese, when worried about the inflation Abenomics may generate, are beginning to convert their depressed Yen into gold.

Tanaka Kikinzoku is a precious metal specialist, owning several large gold shops in Japan. He said in a recent interview that March was the busiest month in the 120 years of history for his company (we presume this is from records and not that he is a modern day near Noah and 120 years old!!). In one of his biggest stores, people have been literally queuing round the block to buy gold ingots. The company has experienced a rise in sales over 500% in many of its stores.

While Japan is relatively unimportant in the global bullion market, with Abe’s bold actions impacting prices at the margin and China continuing to consume, we fail to see our friends at Goldman Sucks prediction of sub $1000/oz prices this year coming to fruition.

If expectations of another round of QE in Japan come to pass before 2014 is out, the case of too much money creation resulting in the relative price of its currency needing to come down will likely add another fillip to her exporters and increase demand for gold. Both the Nikkei and the gold price (certainly the latter in Yen) are highly likely to rise under this scenario.

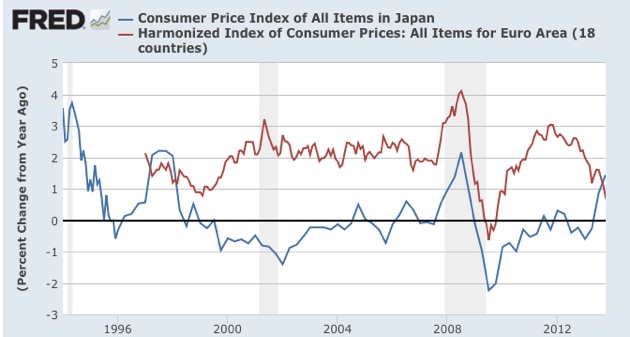

In the meantime, newly resurgent inflation in Japan is contributing to the deflationary forces in Europe with the European’s now importing the 20-years of deflation Japan had.

The ECB has done a relatively good job at keeping prices stable in the aftermath of the financial crisis as the chart below relays aswell as the role reversal taking place between Japan and Europe in their respective inflation trends.

Mario Draghi has been resisting in recent months the temptation to restart quantitative easing but rhetoric last week at the post ECB meeting conference shows that he may once more be forced into action.

In our Titan Global Macro fund we are presently long Japan via outright futures and also long gold miners via the main ETF (GDX) and selected gold plays aswell as through various option strategies. With gold down near 8% in the last few weeks, and sentiment stacking against it once again while Japanese equities have also been unloved this year, we think the chart below tells a different story.

We are happy to see these larger macro trends play out and believe our approach is a “either heads or tails we win” in the way we have structured our portfolio. Either way, the chart of the Nikkei above is not, in our long experience, one that looks like it is going lower.