Richard Jennings of Titan Inv Partners

It is, sadly, a rainy day (not in Georgia!) in God’s Own County today (that is Yorkshire of course!) and what better activity is there than in the peace of the weekend without the freneticism and distractions of the markets than to reflect upon the state of play in our favourite subject? Yes, you guessed it – Precious Metals!

It doesn’t seem like it to many, but gold is in fact one of the better performing asset classes so far in 2014, outperforming the S&P by around 7% in fact. Oddly however, silver is actually down on the year. Many people believe that silver is a sort of turbo charged play on gold. Well, if so, somebody forgot to hit the turbo switch! Notwithstanding this being Zak Mir’s monthly pick for this month (see here on page 54 – http://issuu.com/spreadbetmagazine/docs/spreadbet_magazine_v28_generic) the metal is resolutely declining to stick to the script.

It was in reading this story here on Bloomberg – http://www.bloomberg.com/news/2014-05-01/silver-looks-like-gold-as-slump-defies-more-car-part-use.html – that my near 20 years experience in the markets had my BIG opportunity antennae twitching…

Here are the important points that I took out of the article –

1. Silver demand is at a 9 year high, and rising with expectations of increasing global growth

2. Analyst price expectations are neutral/bearish.

3. Silver declined 36 percent in 2013 – the largest since 1981 which was in the aftermath of the infamous Hunt Brother silver squeeze – http://en.wikipedia.org/wiki/Nelson_Bunker_Hunt

4. Hedge funds have cut their long position by 90% over the last 2 months and in fact now hold 2,620 long futures exposure against a 5 year average of over 20,000.

5. ETP holdings and retail demand for silver coins and eagles remains very healthy.

6. Volatility is deterring investors from entering the market.

7. The Gold/Silver ratio is at an important high and previously an inflection point.

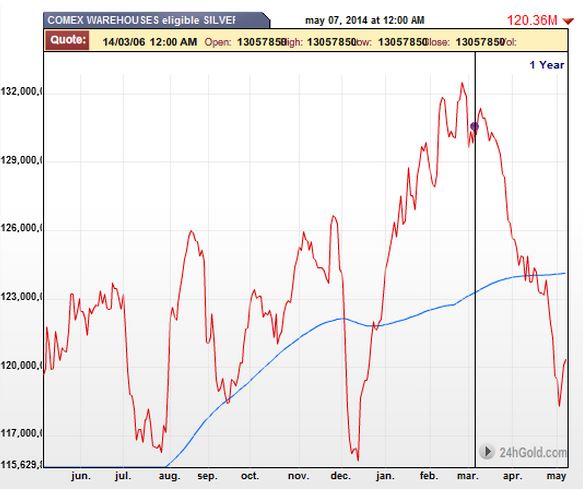

Dealing with some of these in turn. It strikes me as odd that industrial demand is at a multi-year high and also physical demand for eagles and coins and ETP’s and yet the price of silver continues to decline. Two charts below displaying the available silver at the COMEX and Shanghai Futures Exchange tell a thousand words and bear out the limited supply conditions (that is, strangely in conflict with an element of the Bloomberg story it has to be said).

Consensus so called “expert” opinion is that prices are going lower, with “The Squid” aka Goldman Sachs and whom, like a certain other stock “tipster”, I ALWAYS like to trade against. I have learnt that when price expectation is one way, the very vast majority of the time prices move the other way. Trick is finding your entry point to trade against the consensus of course and position sizing appropriately.

Hedge funds hold one of the smallest long positions on record. This is very important to a contrarian investors as at first flush it would appear that the so called “smart money” not being enthusiastic about the metal is a bearish sign. The chart below shows just how “smart” the hedge fund spectrum has been over the last few years.

Indeed, in recent weeks it was reported that hedge funds had their worst month for nearly 13 years as the tech sector got routed. For many of these funds, “hedging” doesn’t seem to enter the equation. What they really are, are levered beta chasers that jump on the momentum trend – great when it keeps going, bad news when it breaks. For us contrarians, the signal here is that should the trend turn and begin to follow the fundamentals, then the bull is NOT presently “in” and the real marginal buying firepower is ready to be deployed.

The volatility issue is also interesting as this reduces the number of participants in a market. Most punters and retail traders prefer to jump on a seemingly steady uptrend rather than trade one that gyrates around dramatically. The comment from the Bloomberg article that silver experienced a dozen bear markets in just 10 years (that is a price decline of 20%) is telling. Equally however if you are nimble and able to recognise the classic signs of a bottom then the rallies can very sharp and so lucrative.

Now let’s look at the latest COT positioning by investors.

We can see that so called “managed money” has a net long position of just 3600 contracts (green block). This is positively miniscule. The producers have also reduced their natural net short position. With the price of silver extraction on an “all in cost” basis widely accepted to be around $21/oz, then the apetite to (a) sell production here, let alone lower is only likely to continue to diminish and (b) with reduced supply due to the loss making economics in the medium term, only add to the very positive supply/demand dynamics for silver going forward.

Here is the chart of the gold silver/ratio that we pick up on below with the key take away’s written into the chart:

So, to conclude, we have silver demand at a multi-year high and this demand is expected to continue to increase over the next few years, our friends the “anal”-ysts, as ever looking through the rear view mirror and acting like most other market participants, that is being conditioned by the price action that has happened rather than looking forward and smelling the aroma of a bottom. The metal is actually the most oversold it has been in over 30 years, and now sitting on strong long term support. It is under owned and unloved by financial market participants (but not in the physical buying capacity) and there are few articles by pundits advising you to buy. Warehouse stocks of the physical are at extremely lows levels and finally, the long term gold/silver ratio is back towards its upper extremes over many years as we highlighted here – https://www.spreadbetmagazine.com/blog/titan-inv-partners-the-goldsilver-ratio-and-what-it-may-be-t.html and that has frequently proved a precursor to sharp rallies.

I’d be hard pressed to find more bullish ingredients for the long silver cocktail that we have here…

So what is going on? Why is silver not rallying with gold? Short answer is we do not know, and anybody who says they do is plain guessing. It is simply counterintuitive to see rising demand and falling stocks and the yet the price of silver continue to remain in the doldrums although there is one very important technical element to pay heed of from the price action in recent months. That is that after hitting a closing low in June of last year of $18.53, the precious metal has, so far, refused to take this out. It came pretty close just over a week ago after the US Non-farm payrolls figure – toeing $18.60 – but then rallied very sharply by over a dollar during the day – what is known as an outside reversal day (going lower than the prior day then taking out the previous day’s high). Not only for Zak Mir (!), but in the face of the fundamentals relayed here, that is an important signal for bulls of silver. We really wonder where the firepower would actually come from to push the metal lower knowing that this would very likely only exacerbate the very tight supply/demand dynamics presently at play.

The likely culprit for the price weakness is the ongoing tapering of the QE bond buying program in the States. With us just over half way through the tapering process and coupled with the extreme oversold status on a long term basis, we would argue that this is now “in” the price. The old adage “buy the rumour sell the fact” could equally be twisted in this case to – “sell the anticipation and buy the closure” (of the bond buying that is).

I leave you with one final chart (see below).

This is the price of silver over the last 38 years. It is the most oversold it has ever been during this period. It is however sitting on old resistance that per technical theory becomes new support. This measure of oversold-edness however is very rare and it is a brave man that goes short here in our book.

How to play a move to the upside then? Well, first thing is to remember that there are no guarantees in the market and they are set up to confound and throw egg on the faces of as many people as possible as much as is possible! There is always the potential for another lurch lower just to really grind the bulls into the dirt – perhaps to $16/oz per the chart above. We will plan for such an eventuality here at Titan through selling puts on a downtick and keeping our position size appropriate in the outright silver commodity/related instrument like the USLV.

For more information on the only Precious Metals fund that is housed within a spreadbetting structure and where all returns are tax free, click the image below.

You should not take this piece as an advocation to trade in any of the instruments mentioned and should always take professional advice in relation to your own personal circumstances.

All Titan Funds operate within a spread betting account which means gains or losses are currently free of tax. However, legislation can change in the future. Spread betting is a leveraged product which could result in losses of some or even all of your initial deposit. Ensure you fully understand the risks.